Merchant Acquiring Strategies: Adapt and Grow in Challenging Times

It only took a couple of weeks for COVID-19 to change the world and force people, businesses and entire industries to adapt on the fly. Across the globe, there is a dramatic decline in POS transactions and a hurried shift to everything digital. It has presented new challenges to merchants and payment service providers alike.

We at OpenWay have been monitoring innovative merchant acquirers and how they are coping with the situation and adapting their payment systems to the new reality. The list of players who rely on our Way4 Acquiring platform includes Asia Commercial Bank, areeba, Worldline, Equity Bank Group, Halyk Bank, and Network International. Their coping strategies and business insights have contributed to this case study, which explores:

Acceptance methods that merchants can afford even during crisis and recession

Five emerging revenue niches in payment processing

What technology an acquirer can offer to the government agencies who are now struggling to optimize and digitize the distribution of social benefits

Ways to monetize collaboration within marketplaces

How acquirers of cross-border payments can compensate for the overall drop in their transactions, and more.

1. No quick cure for the economy

According to McKinsey, the quarterly global GDP in the second quarter of 2020 could decline by as much as 35 to 40 percent. The manufacturing industry is enduring a significant drop of end-user demand, supply-chain disruptions and plant closures. Oil prices have been sent crashing to their lowest level since 2001, and gas demand has fallen by one-fifth in some cases. Hospitality and tourism have seen the most significant impact, with an almost complete shut-down in activity and bookings in many world regions.

At the same time, certain technology-advanced businesses have hit the jackpot. For the online communication platform Zoom, user numbers have leaped from 10 million to more than 200 million people a day. E-сommerce retailers and related supply chains are experiencing triple-digit order and revenue growth. The cloud gaming industry is also on the rise: for example, the gaming platform Playkey reports 300% revenue growth.

"In every hardship, there lies an opportunity to envision and create a brighter future. We firmly believe that after the COVID-19 outbreak, service providers who are able to tap into the power of digital technologies will come out the strongest." Simon Hu, CEO of Ant Financial

“Technology has become a GVC (great virus crisis) staple, right up there with food and toilet paper”. Ed Yardeni, President and Chief Investment Strategist of Yardeni Research Inc.

In most cases, staying afloat now means re-building internal processes and relying on technology more than before. How long will it take a company to adapt to the new realities? The speed of adaptation is directly linked to the company’s core IT platform and whether it’s ready to change.

2. Merchant acquiring in crisis - stats and trends

Retail payments and merchant acquiring business appear among the worst hit. Already, in the middle of March 2020, foot traffic to stores was down by around 20 percent in the UK and by more than 70 percent in Italy and the US (compared with the same period last year). Payment volumes on POS could drop as much as 30-40 percent in the short term, McKinsey predicts.

The payment wallet industry is also affected, with some leading apps in Asia reporting 20-30% less flows, despite the growing number of users.

Acquirers are under unprecedented pressure and taking unprecedented steps in this uncertain time to relieve pressure on their merchants, especially on the small and medium businesses. One trend is the elimination of acquiring fees.

Areeba, the leading processing company in Lebanon, is waving the monthly rental fee of POS terminals and offering free installation. Ramzi Saboury, areeba’s Chief Commercial Officer, said: “Business owners in Lebanon faced tremendous pressure on their business revenue. areeba’s main objective from this initiative is to help merchants in Lebanon in managing financial challenges that have surfaced from the COVID-19 outbreak. We want to offer support and help them in the ways we can, not just financially but morally as well.”

Network International, the leading merchant acquirer in the Middle East, is waiving minimum monthly service fees for all merchant clients in the UAE across all industries for the next three months. Samer Soliman, Managing Director for Network International’s Middle East operations, said: “We recognise that some of our merchant partners have been severely impacted by this extraordinary situation and we are standing by those that need us most, with immediate and practical relief measures over the next few months.”

Is this generosity only for major players who process large volumes of “on-us” transactions without interchange fees? Or could any acquirer reduce the acceptance costs for its merchants while not causing its own revenue decline? The answer depends on the flexibility of the acquiring platform and if it can accommodate alternative acceptance methods.

3. Very affordable alternative to POS terminals

One of the alternative acceptance methods, both hygienic and cost-efficient, is QR code payments. It is particularly suitable for merchants who cannot afford a POS terminal. OpenWay clients have implemented the QR code technologies of all major payment schemes, including Alipay, Masterpass QR or UnionPay QR, also domestic schemes.

Most such projects work in the merchant-presented mode, where a merchant prints the QR code and buyers scan it with a phone. This method is the easiest and cheapest to implement. Some projects also work in a customer-presented mode. In this case, a merchant uses a mobile device with special payment application to scan the QR code on the buyer’s screen.

Halyk Bank, serving 74,000 merchants in Central Asia on the Way4 platform, introduced VISA Scan&Pay QR code service in 2018 as part of their expansion into the SME and transit market. Their merchants began to printout QR codes and display them in their stores as a payment alternative, with merchant charge of just 1% per transaction. Compare this to an investment of 250 US dollars, the average price of a POS terminal in the region, and 2.7% merchant charge for Visa transaction at a classic POS terminal.

Halyk Bank has helped its merchants to cut costs before, when in 2013, it became the first in Central Asia to offer an mPOS service for only 20 US dollars per device – 6 times cheaper than a POS terminal. The merchant service charge was only 2.6% per transaction, 10 cents lower than the fee charged by Square, an mPOS pioneer at that time.

Transit payments via the Halyk Bank’s app in Kazakhstan

4. Compensate for empty stores with omni-channel

The long weeks of social distancing have fueled the adoption of contactless and online payments. This trend is promoted by card networks, governments and major financial institutions. Mastercard alone has enabled up to 200% limit raise for PIN-less contactless payments in 29 European countries. Central Bank of Russia has required banks to limit the e-commerce acquiring commission to 1% – that is cheaper than typical POS acceptance costs and motivates merchants to prioritize sales via web and mobile. Major acquirers globally are taking steps in the same directions decreasing fees for online acquiring. They offer hugely discounted pricing and free advice on how to build a payment journey for Internet shoppers.

Network International has waived fees for online acquiring for the new SME customers for three months to help them quickly enable their business online. Major acquirers globally are taking steps in the same directions. They offer hugely discounted pricing and free advice on how to build a payment journey for Internet shoppers.

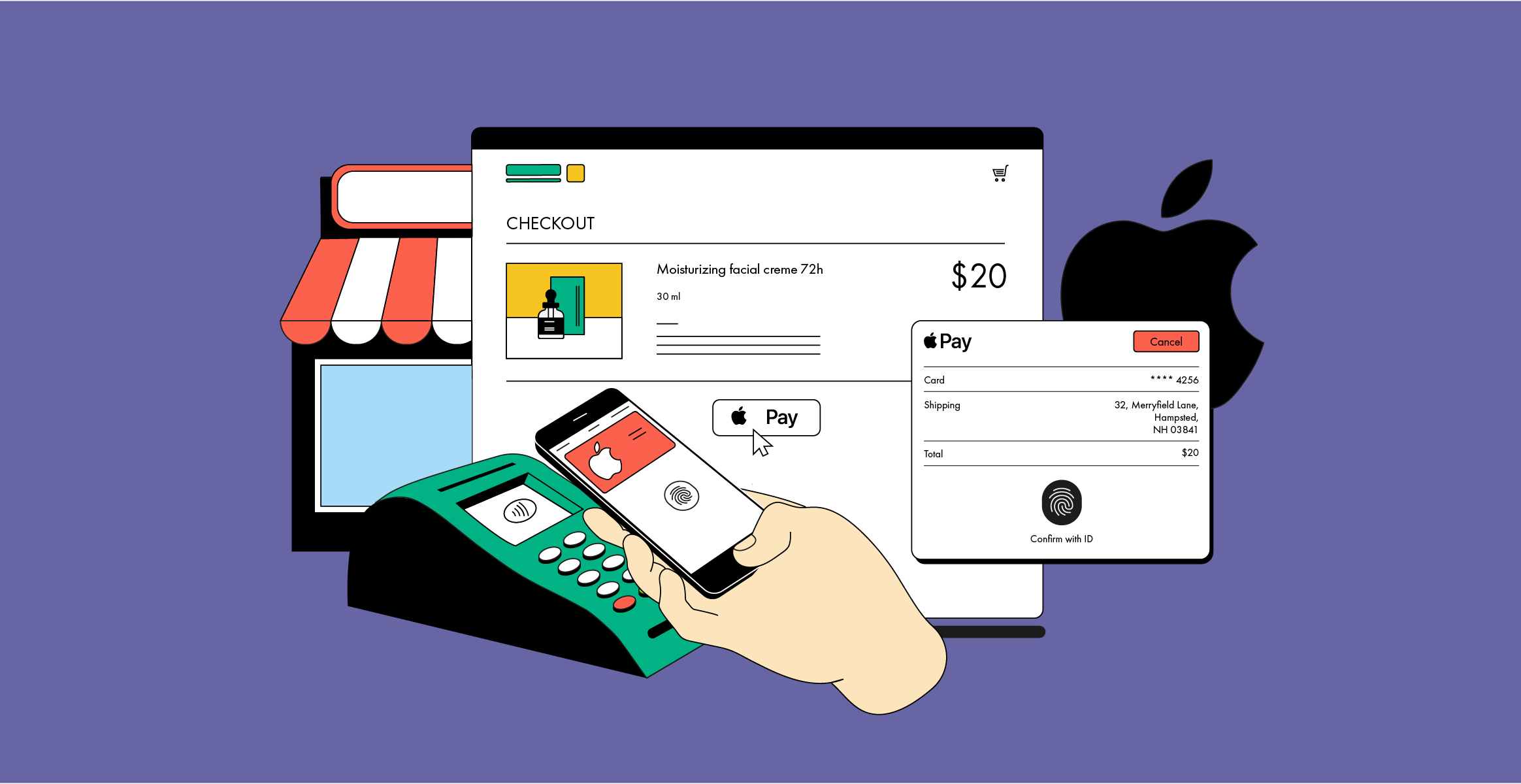

All the above will speed up the adoption of mobile wallets that are accepted both in-store and online – such as Apple Pay and Google Pay.

Now acquirers are expected to enable digital payment methods as soon as possible. It would be a strong competitive advantage to add the “true omni-channel” label to their offering. With many shopping malls now closed, the consumer journey starts with retailer websites and m-commerce apps and finishes in designated pick-up points. Those who provide a seamless payment experience has higher chances to expand its portfolio of online merchants.

Another competitive advantage is to be prepared for the increased load on digital infrastructure after people shifted from social outings to social distancing. To avoid outages in online payment processing, acquirers can deploy high-availability solutions. Some of our clients implemented Way4 even on the cross-Atlantic scale: even if their authorization system in Europe gets down, transactions would be routed to the backup online system in the US. It guarantees that a payment initiated by a consumer is completed anyway.

5. Offering the best acceptance fee

Example by Credit Card Compare: The cost of accepting 23 payment options in Australia

Mastercard and Visa are the most widely accepted payment means, but the related merchant service charge is a burden for the SMEs who process low transaction volumes. Acquirers can offer these merchants multiple alternatives with a lower per-transaction fee. Usually, payment acceptance is cheaper for local card brands, domestic mobile wallets, and direct bank transfers. Some payment methods may even provide a faster or instant settlement.

For example, for a purchase of 50 euros from a merchant in the Netherlands, these acquiring fees can be expected for these acceptance methods (estimated):

0,35 euro for iDeal, an interbank scheme, the most popular payment method domestically (0.25 euro + service fee)

0,35 euro for SEPA direct debit transfer (0.25 euro + service fee)

0,5 euro for Mastercard (average interchange++ total 0.90%-1.10%)

1,97 euro for UnionPay or Discover (3.75% + service fee)

So for this transaction, iDeal or SEPA direct debit would be the preferable acceptance methods for the merchant. At the same time, if the purchase total is under 10 euros, accepting a card payment would be more economical than using alternative payment methods.

When the acquiring platform dynamically adapts to the customer and transaction context, and is able to highlight the most cost-effective acceptance method, merchants enjoy more cost savings. This in turn increases their loyalty to the acquirer.

Another example of a cost-effective acceptance method is QR code payments in Russia offered by a brand-new domestic instant payment scheme (Fast Payments System). According to the scheme, merchants pay a third of the cost of accepting a card payment.

The affordability and simplicity of in-app payments was one of the success drivers of SmartPay, a domestic closed-loop wallet scheme in Vietnam. It signed up over 250,000 SMEs and 585,000 consumers in just seven months. Using our Way4 platform, SmartPay built an ecosystem of 100% cashless and instant payments. When a buyer scans the merchant QR code, the money is credited to the merchant’s account instantly. It helps SMEs replenish their stock and invest in business growth quicker.

QR code displayed by SmartPay merchant at the local market in Vietnam

For multiple acceptance methods, the preferred scenario is when all clearing and settlement is handled by one system. It helps acquirers to avoid interfaces redundancies and keep their payment processing more transparent.

6. Dynamic multi-factor merchant pricing

Due to the combination of different acceptance methods, channels and regions, the pricing management may be a challenge for acquirers. It takes a highly flexible tariff engine to ensure that every merchant gets an optimal offering. Here are some examples of the required flexibility supported in Way4:

Configuring fees depending on the merchant size: the simplified fixed pricing for a stable SME; the interchange-plus model for big retailers; and for a growing startup – the dynamic pricing based on the mix of total transaction value and average transaction size.

Adjusting to the merchant’s business conditions in real time: waiving the terminal rental fee if the monthly gross sale total was less than a certain amount, or giving discounts to those using online and touch-free acceptance.

Applying special rules in bulk to a group of merchants – for example, decreased fees for all merchants selling essential goods in the areas hit by drought.

One of our clients works with over 40,000 merchants and offers personalized pricing to each. This acquirer company saves much time and money by configuring all tariffs on its own, without heavy customization or vendor involvement. Their pricing schemes in Way4 can be based on over 30 transaction factors. The system can even analyze the shopping cart items in real time and charge the transaction fees or apply discounts accordingly.

With pricing diversity comes complexity in revenue calculation. How can acquirers keep a healthy balance between competitiveness and profitability? What’s the lowest merchants service fee that still makes sense for the acquirer? There are several business intelligence tools that predict acquiring revenues. Way4, for example, allows acquirers to measure the profitability of every individual account in their portfolio.

7. Five revenue niches that acquirers can explore

With less foot traffic to merchants and their need of financial reliefs, the conventional acquiring revenue based on the merchant service charge is in decline. Some acquirers are compensating for these losses through these innovative business models:

Currency exchange for cross-border payments

MCP service allows online merchants to price their goods in different currencies depending on the buyer’s location.

Due to travel bans and self-isolation, people are shopping mostly online. Statistically, they are 20% more likely to buy the product if allowed to pay in their preferred currency. Acquirers support such transactions with two services – dynamic currency conversion (DCC) and multi-currency pricing (MCP). When the purchase is complete, the merchant and acquirer can split the conversion markup between themselves.

In-store and e-commerce consumer instalments

Merchants can get instalment plans for the consumer for any purchase on the fly via APIs to the Way4 loan management platform.

A joint acquirer-merchant consumer finance program can support merchant sales at the time of crisis. Way4 enables buyers to get instant instalment loans – whether on POS or during e-commerce checkout. Acquirers can set up a special fee for each instalment-based sale.

Marketplace ecosystems

An acquirer that has grown its business to the state of a multi-player ecosystem has more leverages to pull itself and its customers out of crisis. This has been demonstrated recently by Alipay. As part of post-pandemic support to the Chinese city Wuhan, a new page appeared in the Alipay mobile menu. It lists Wuhan businesses and enables purchase of their products and services right in the app. While those merchants can recover sales faster, Alipay gets more revenue from the related payment processing.

Another example is SmartPay, mentioned earlier. This Vietnamese mobile wallet has connected SMEs and consumers, on one side, and the country’s largest consumer finance company FE Credit, on the other side. Through a special menu, the app users can apply for loans and get the funds instantly to their wallet account. Their purchasing power increases, and it has a positive impact on SmartPay’s processing volumes.

Such marketplace ecosystems benefit all parties. Businesses connect to potential customers and partners faster and at a lower cost; consumers get more options to choose from; and acquirers charge a commission for each deal that happens on the marketplace. To ensure these benefits, the acquirer’s platform has to support multi-level hierarchies of participants and comprehensive settlement schemes. For example, in Way4, the system applies due fees automatically to instalment-related transactions and distributes the funds among the merchant, marketplace owner, payment gateway and instalment provider.

Social benefits programs

The acquiring of social welfare cards can be a business opportunity with many benefits. Enabling subsidized purchases helps businesses to position themselves as socially responsible and strengthens thier ties with local authorities.

Way4 Social Cards is a digital solution for social payment distribution which supports basket data analysis

Additionally, if the acquiring system supports basket data analytics, it can be used in projects that improve consumption habits among the population. For example, during times of crisis gambling and alcohol spending may rise. Our Way4 platform analyses purchases in real time and declines them if restricted items are detected. On the other hand, it can apply discounts to subsidized items like medicine or child care products.

Merchant financing

After the US government offered coronavirus relief loans to its SMEs, JP Morgan Chase received 60,000 applications in five minutes. “It was Hunger Games,” commented one banking executive when the dedicated fund ran out of money too soon. Many financial companies are now following suit and entering the merchant financing market to meet the increased demand. This niche may generate significant additional revenue for acquirers.

In case of revenue-based financing, merchants apply for it online, and the acquirer can make due checks before granting approval. A merchant who receives funds will be charged monthly repayments in proportion to its revenue for that month. It is important that the acquirer is able to re-adjust the loan terms in the system – for example, refinance it or setup payment holidays for debtors most affected by crisis situations.

Our clients who use Way4 both for acquiring and issuing can provide financing in the form of purchasing cards for the merchant’s employees. These cardholders get instant access to credit funds. The merchant, of course, can set various spending limits and configure which goods each employee may and may not purchase. The accounting becomes digital and simplified, as cash is removed from the process. The acquirer can charge a fee for each of these value-added services.

The modular architecture of the payment platform will be an advantage for a payment company that wants to generate more revenue streams by offering advanced technology to customers and partners. Acquirers who use Way4 can expand into new business areas by connecting additional Way4 modules such as card issuing or loan management.

8. How to reduce operational expenses

To stay cost-effective during the crisis, companies are optimizing not just revenue models, but also internal operations. Acquirers can reduce the probability of internal fraud and human error by automating key payment processing routines – merchant onboarding, payment acceptance, chargeback management, clearing and settlement, risk monitoring and more.

With the growing number of digital payments and external systems involved, it takes advanced technology to keep risk monitoring consistent across all channels. The Way4 Intelligent Fraud Prevention solution automates the analysis of over 150 parameters in transactions coming from any acquiring interface. It applies fraud-preventing restrictions in real-time – this is the key to reducing chargeback cases for merchants and saving money for acquirers.

Way4 Intelligent Fraud Prevention solution is a multi-channel, multi-system solution for merchant acquirers to monitor and prevent fraudulent transactions.

For most industries, the shift to automated workflows provides one more benefit – an improved customer experience. Our clients confirm that they have become more attractive as acquirers after launching 24-hour digital merchant onboarding and real-time merchant support via online portals.

9. Why waiting out the crisis is not an option

It is tempting to foster an illusion that the worst is behind us and everything will return to normal soon. Experts say that it will not: the impact on customer expectations and behavior and those of businesses is too intense, and payment players will have to deal with “the new normal”.

“Payments today are a major cost burden for many banks, and most spending maintains existing systems instead of creating change. In the postcrisis world, banks will need to reflect on how to organize themselves for change, possibly by running some of their payments businesses in a completely different way. They could, for example, consider structural moves on the use of onshoring versus outsourcing, cloud-based infrastructure, automation, and analysis-driven decisions to reimagine scale or the realignment of products.”

From “How payments can adjust to the coronavirus pandemic—and help the world adapt”, an article by McKinsey’s analysts

For acquirers, the COVID-19 crisis is an opportunity to test their payment infrastructure. How well is it prepared for the new market? Will it compensate the reduction or loss of traditional revenues by generating new ones? According to technology consultancy Omdia (formely Ovum), legacy system modernization and creating digital capabilities were the top imperatives for financial institutions in the beginning of 2020.

Key technology trends driving retail banking in 2020 by Omdia

10. Why acquirers keep relying on Way4

This crisis is unlikely the last one in modern history, and no one knows how much time is left to prepare for the next blow to the market. This is why our clients require that we equip every Way4 solution with technologies that help them survive long-term. They need both - competitive advantages for today and resilient capabilities for an uncertain future.

The Way4 Acquiring solution at a glance

Most of the acquirers using our platform prioritize the same abilities:

- To optimize acceptance costs for merchants by supporting multiple traditional and alternative payment methods.

- To enforce profitability by configuring merchant products and tariffs flexibly, and without the need of vendor customizations.

- To support end-to-end omni-channel payment processing.

- To diversify revenue streams, expanding from mere merchant acquiring to card issuing and digital wallets, thanks to the modular architecture of Way4.

- To save costs by automating multiple merchant acquiring operations, including customer onboarding, risk monitoring, payments, and dispute management.

Another advantage for these times is compliance with social distancing regulations: the option of launching our platform 100% remotely, whether in-house or in the cloud.

11. Learn more: analytic reports, news and case studies

Acquirers on Way4 platform now can serve marketplaces, OpenWay, 26 Feb 2018. Available at: https://www.openwaygroup.com/new-blog/2018/2/26/acquirers-on-way4-platform-now-can-serve-marketplaces (Accessed: 6 May 2020)

Alipay launches recovery assistance for Wuhan merchants, Mobile Payments Today, 9 Apr 2020. Available at: https://www.mobilepaymentstoday.com/news/alipay-launches-recovery-assistance-for-wuhan-merchants/ (Accessed: 6 May 2020)

Areeba to support all its merchants during the coronavirus pandemic, areeba, April 2020. Available at: https://www.areeba.com/english/news-and-events/press-release/areeba-to-support-all-its-merchants-during-the-coronavirus-pandemic (Accessed: 6 May 2020)

Boyd D. Cost comparison: 23 ways to accept payment in 2019, Credit Card Compare, 8 Jul 2019. Available at: https://www.creditcardcompare.com.au/blog/ways-to-accept-payment-chart/ (Accessed: 6 May 2020)

Bruno Ph., Chaudhuri R., Denecker O., Niederkorn M. (2020) How payments can adjust to the coronavirus pandemic – and help the world adapt, McKinsey. Available at: https://www.mckinsey.com/industries/financial-services/our-insights/how-payments-can-adjust-to-the-coronavirus-pandemic-and-help-the-world-adapt (Accessed: 6 May 2020)

Columbus L. (2020) How COVID-19 is transforming e-commerce, Forbes, 28 Apr 2020. Available at: https://www.forbes.com/sites/louiscolumbus/2020/04/28/how-covid-19-is-transforming-e-commerce/#1016df453544 (Accessed: 6 May 2020)

Crawford Sh. (2020) How can your industry respond at the speed of COVID-19’s impact? EY, 8 Apr 2020. Available at: https://www.ey.com/en_ly/covid-19/how-can-your-industry-respond-at-the-speed-of-covid-19s-impact (Accessed: 6 May 2020)

Fetisov V. (2020) Russia experiences unprecedent growth in cloud gaming, 3D News, 23 March 2020. Available at: https://3dnews.ru/1006880 (Accessed: 6 May 2020)

Full list of prices for supported payment methods, Adyen (2020). Available at: https://www.adyen.com/pricing/full-list (Accessed: 6 May 2020)

Mastercard enables contactless limit raise across 29 countries; and champions permanent increase, Mastercard, 25 Mar 2020. Available at: https://newsroom.mastercard.com/eu/press-releases/mastercard-enables-contactless-limit-raise-across-29-countries-and-champions-permanent-increase/ (Accessed: 6 May 2020)

Mayo D. Evaluating the impact of COVID-19 on retail banking technology, Accelerating the shift to digital, Omdia, 7 Apr 2020.

mPOS terminals are six times cheaper than traditional terminals, Forbes, 25 Dec 2013. https://forbes.kz/finances/finance/mpos-terminalyi_v_6_raz_deshevle_traditsionnyih/ (Accessed: 6 May 2020)

Network International announces AED 5 million in support measures for UAE merchant partners, Network International, 24 Mar 202. Available at: https://www.network.ae/en/news/view/network-international-announces-aed-5-million-in-support-measures-for-uae-merchant-partners (Accessed: 6 May 2020)

OpenWay launches multi-currency pricing solution for global acquirers, OpenWay, 27 Sep 2017. Available at: https://www.openwaygroup.com/new-blog/2017/9/27/openway-launches-multi-currency-pricing-solution-for-global-acquirers (Accessed: 6 May 2020)

Popken B., Ruhle S. Small-business loan program ran out of money within minutes, some banks say, NBC News, 19 Apr 2020. Available at: https://www.nbcnews.com/business/business-news/small-business-loan-program-ran-out-money-within-minutes-some-n1187051 (Accessed: 6 May 2020)

SmartPay and OpenWay target market potential 25M consumers and 6M SMEs with their financial inclusion wallet in Vietnam, OpenWay, 26 Jun 2020. https://www.openwaygroup.com/new-blog/2019/6/26/smartpay-and-openway-target-market-potential-25m-consumers-and-6m-smes-with-their-financial-inclusion-wallet-in-vietnam (Accessed: 6 May 2020)

Two QAZCOM innovative products have been awarded by the Big Four international experts at a time, OpenWay, 19 Jul 2018. Available at: https://www.openwaygroup.com/new-blog/2018/7/19/two-qazkom-innovational-products-have-been-awarded-by-the-big-four-international-experts-at-a-time (Accessed: 6 May 2020)