Merchant acquiring profitability: a piece of cake or a pig in a poke?

Ilya Dubinsky, VP CTO Office at Credorax

Credorax (now part of Shift4) is an innovative award-winning European merchant acquiring bank serving global e-commerce merchants and PSPs. In addition to his duties at the CTO Office, Ilya is also a contributor to the Berlin Group and author of Acquiring Card Payments.

Marek Forsyiak, CEO at SmartPay

SmartPay is one of the leading financial inclusion wallets in Vietnam. Marek oversaw the creation of a nationwide network covering 700,000 merchant acceptance points comprised mostly of SMEs, acquiring a user base of over 40 million customers initiating over million monthly transactions.

Hermann Tischendorf, Digital Transformation & Innovation Consultant

Hermann is a consultant specializing in IT strategies and digital products in FinTech, PropTech, and InsurTech.

“Vietnam was badly hit by COVID-19. As a result of the lockdown, as many as 25% to 30% of micro-merchants and street vendors have closed. Thanks to our focus on this segment, we ensured that our clients had all the opportunities to survive in these times and replace lost revenues. Financial inclusion wallets like SmartPay can play a big role in these goals. How do we take a traditional offline merchant and bring them online? By adding a real value that allows their businesses to grow! We deliver VAS that allow micromerchants and street vendors to be as successful as the most advanced e-commerce provider. Technology allows for democratization of these processes and we are putting the micro-merchant first. This is why we purpose-built SmartPay from the ground up. We had to think of how to deliver the products and services relevant to SMEs on a cost-effective basis to ensure our ability to succeed in the long term.”

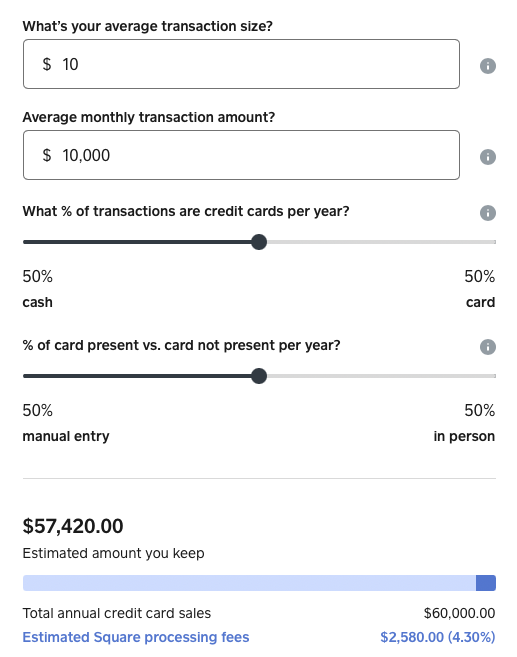

Square fee calculator for merchants. Source: Square website

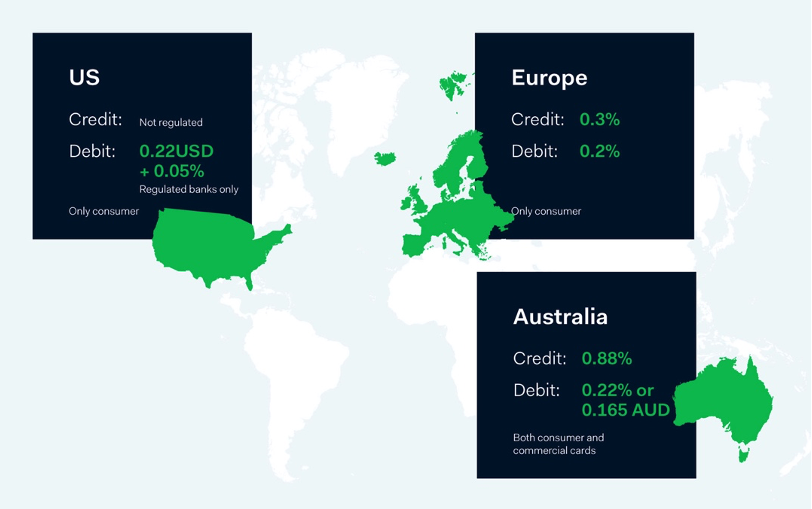

Interchange caps in different countries. Source: Adyen

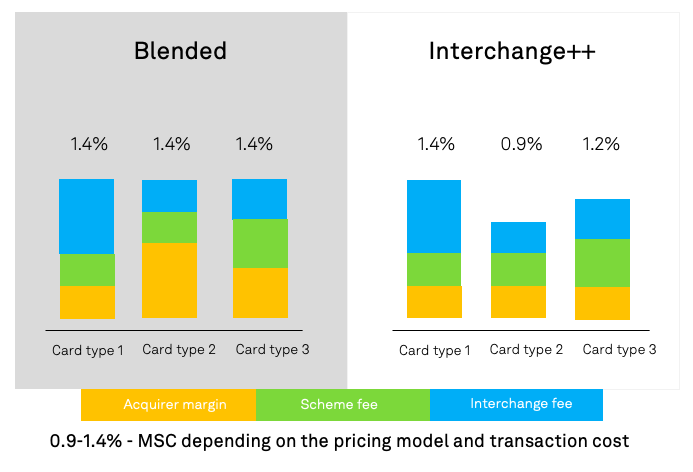

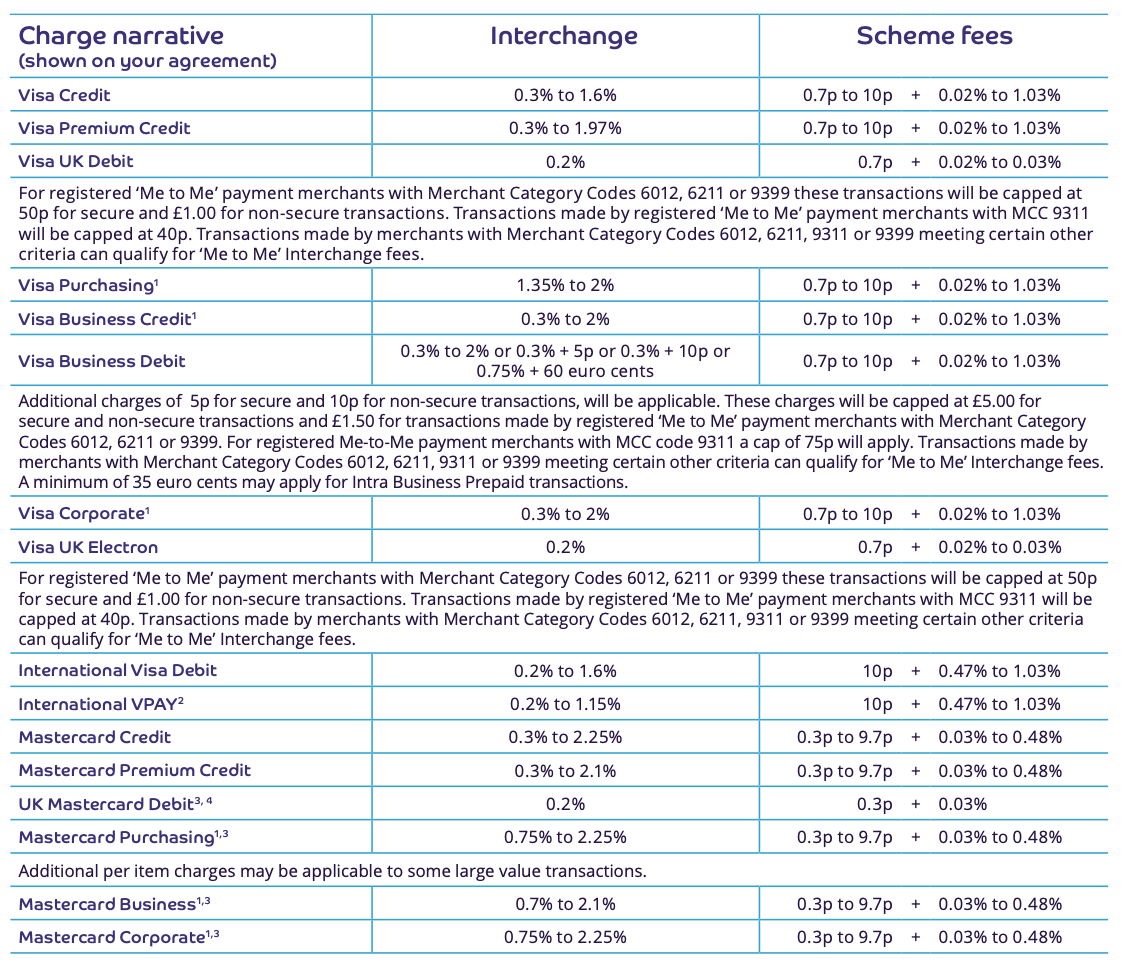

The tricky guide to Interchange rates and scheme fees by Barclaycard.

“Payments is what we would call a hygiene function. No one is making money from payments. It’s something you need to have to enable all the other stuff, a sort of glue holding the whole thing together. Buyer or seller, private individual or merchant, we want to get people out of cash and into electronic payments. So we are providing services that are particularly tailored to the needs of these people. They don’t have access to credit. They don’t have access to savings products. They don’t have the opportunity to open a small web shop and show their products to the world. We are giving them a platform that is doing all this on top of payments.”

“Payments are a service nobody wants to see — customers just want it to happen as seamlessly and invisibly as possible. But to be truly invisible, a payment service must be very reliable, very global and very local at the same time. Which is what we do while adding value for our merchants — multi-currency pricing and settlement, 99.999% reliability, interchange fee prediction, and smart optimization of approval rates.”

“Data increases the value of your services to merchants. You can't let data go to waste!”

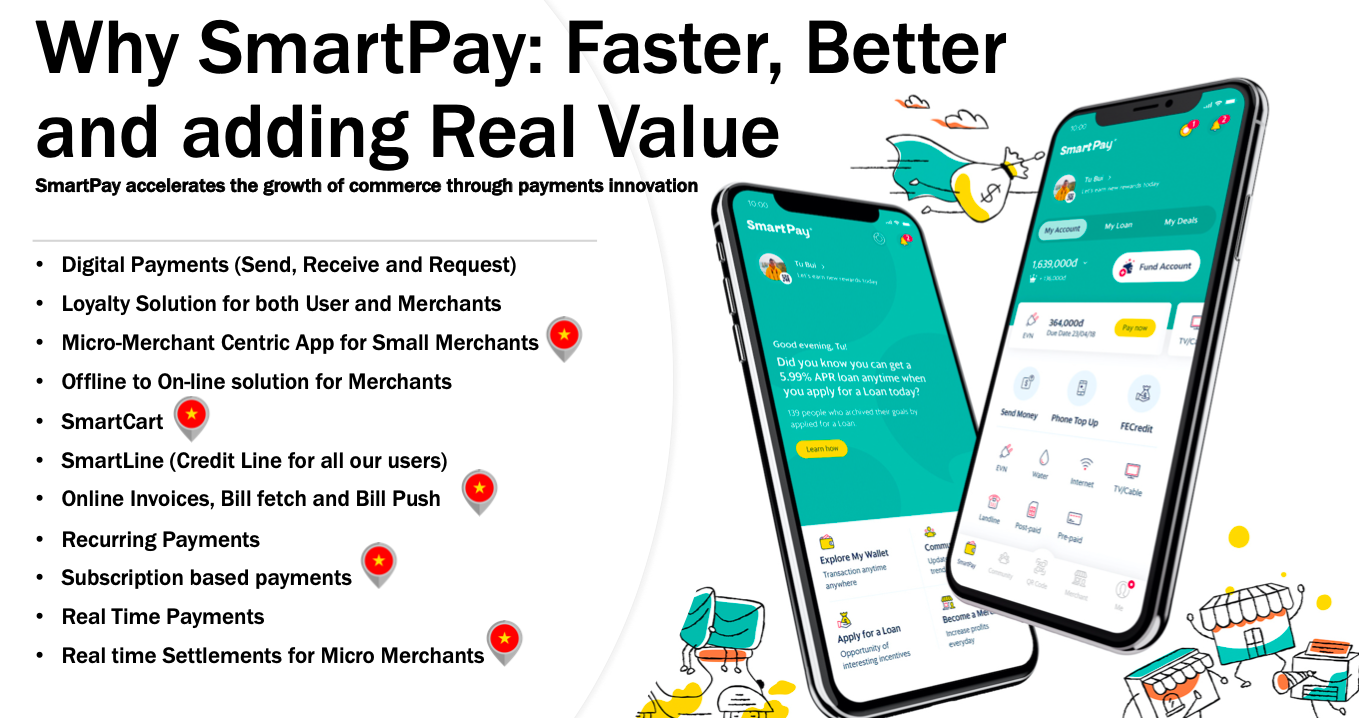

“Real value comes from a platform that’s smarter: smarter in a sense that it understands the buyer-seller dynamics in real-time. Real value comes from adding capital to the exchange. As part of VP Bank, we are leveraging it by offering a credit to the buyer or a working capital to the merchant. Some features that we offer such as SmartCart are unique for Vietnam.”

OpenWay is a best-in-class provider of digital payment software solutions, and the best cloud payment systems provider as rated by Aite and PayTech. OpenWay is a strategic partner of tier 1/2 banks and processors, fintech startups, and other leading payment players around the globe. Among them are Network International and Equity Bank Group in MENA, Lotte and JACCS in Asia, Nexi and Shift4 in Europe, Comdata (a Corpay Company) and Banesco in Americas, and Ampol in Australia.